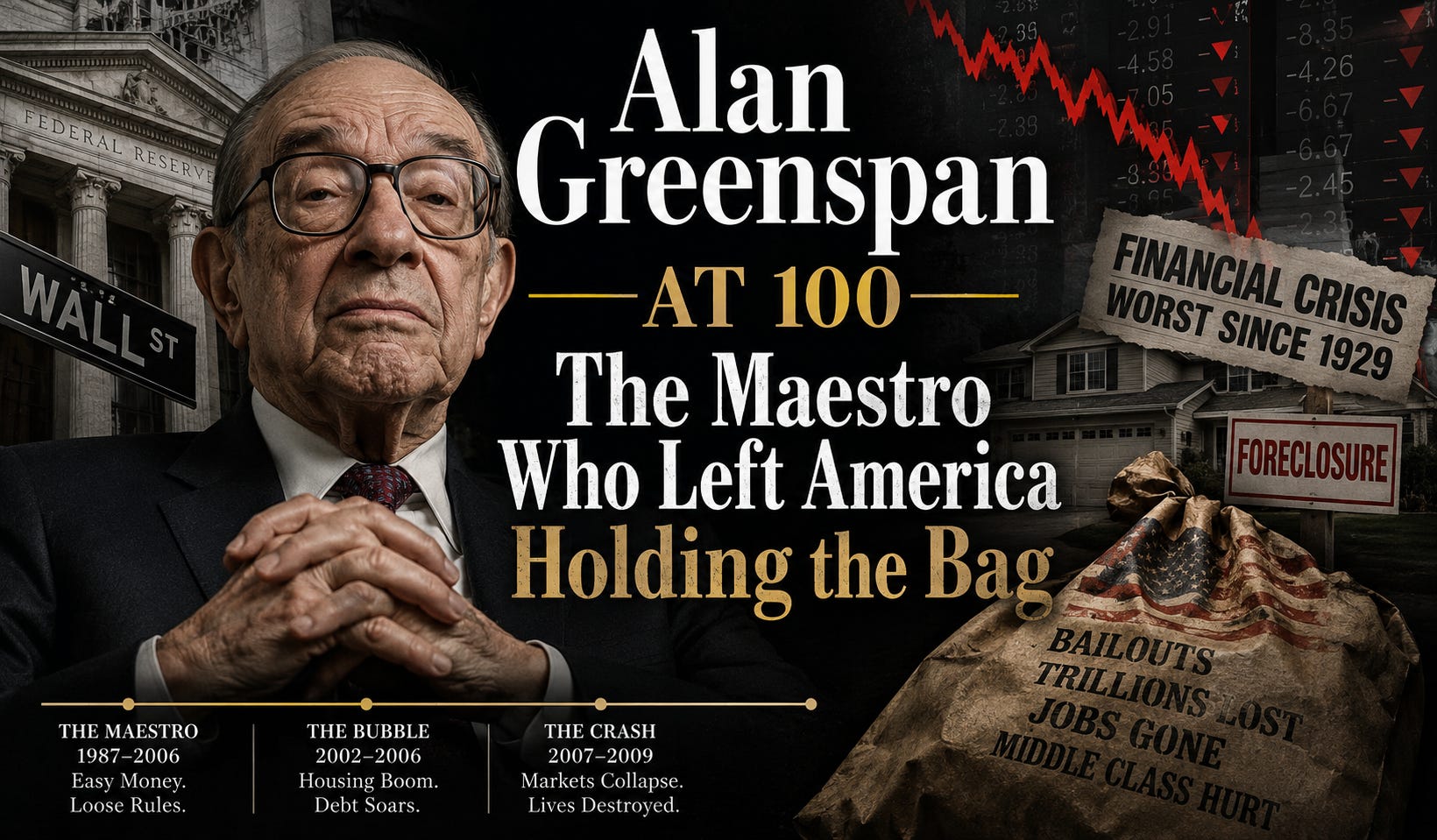

It’s Not Great to Criticize the Dead, but Dying Doesn’t Get You off the Hook

Alan Greenspan, Fed Chairman Through Prosperity and Crisis, Dies at 100

The New York Times tells us “the pre-eminent economic policymaker of his time and a skilled political operator, he favored market-friendly stances that would later come to be associated with destructive financial forces.”

Pre-eminent is defined as “greatest in importance, degree, significance or achievement.” Not quite sure how the NYTimes sqaures that with ‘would later come to be associated with destructive financial forces, but the NYT these days marches to its own drum.

Balderdash.

I had Alan in my sights a full decade before 2008, and long before guys like Greenspan came to understand that, just like night follows morning, ‘what goes up must come down.’

Let me give a few examples:

(From my Nov 29, 2002 article) Alan Greenspan, the Big Man in Finance

“It occurs to me that the big man in finance is not Alan Greenspan or whoever happens to chair the SEC at the moment, not the heads of Wall Street trading firms and certainly not the business moguls who run international companies…

“… My Daddy used to say that the market was made up of “the sheep, and those who shear the sheep.” But Daddy was a creature of the Depression and those were times before such things as institutional investors. What hasn’t changed since the Thirties is the incredible ability of the greedy to find new investment vehicles to support their greed.”

Those of you who follow bank robberies know that a ‘vehicle’ is the getaway car, idling at the curb.

(From my Sep 16, 2007 article) Alan Greenspin Finally Writes His CYA Memoir

“Alan Greenspan was, for a time, one of the more favorably looked-upon Chairmen of the Federal Reserve, an organization only seen as through a glass, darkly. We humans have an imperfect perception of reality and a tendency to make our own when it suits us, particularly at the end of long and contentious lives.

“Presiding over the aftermath of a dot-com bubble he failed to recognize, he retired just before the housing bubble burst, thus avoiding bubble-gum all over his face and yet another blemish to the old career, happening on his watch. Not everyone saw the dot-com mess. On the other hand, everyone saw the housing bubble and the greed of a sub-prime feeding frenzy but Alan, who essentially initiated it for reasons known only to him…

“…Lowering the discount rate to an unprecedented 1% and knowing that would set up a mortgage refinance tsunami, Alan testified to Congress,

“Besides sustaining the demand for new construction, mortgage markets have also been a powerful stabilizing force over the past two years of economic distress by facilitating the extraction of some of the equity that homeowners have built up over the years.”

Stabilizing was it? Extracting homeowner equity?

(my article continues) “That ‘extraction’ has worked to destroy families, wreck retirements, suck dry the single largest economic pool supporting most American homeowners, leverage an already overheated personal debt ratio and cause the greatest percentage of foreclosures since the Great Depression. Alan singlehandedly transferred economic distress from businesses to individuals…

“…In April, 2005 the great man pontificated,

“Innovation has brought about a multitude of new products, such as subprime loans and niche credit programs for immigrants. Such developments are representative of the market responses that have driven the financial services industry throughout the history of our country … With these advances in technology, lenders have taken advantage of credit-scoring models and other techniques for efficiently extending credit to a broader spectrum of consumers. … Where once more-marginal applicants would simply have been denied credit, lenders are now able to quite efficiently judge the risk posed by individual applicants and to price that risk appropriately. These improvements have led to rapid growth in subprime mortgage lending; indeed, today subprime mortgages account for roughly 10 percent of the number of all mortgages outstanding, up from just 1 or 2 percent in the early 1990s.”

If bullshit was music, Alan, your ass would be a whole brass band.

I wrote in that essay that

“Credit-scoring models such as filling in your own mythical annual salary without additional substantiation. Judging the risk by not asking how much debt is already owed by the mortgage applicant. With advantages in technology like lender-abetted lies and subterfuge, banks hired ‘loan specialists’ who were paid by commission like used car salesmen.

“Everybody in Greenspan’s co-conspiracy made a buck on the ‘front end charges’ to these borrowers of last resort, then packaged their bad loans off to someone else, who repackaged them again to specialty hedge funds.”

I rest my case.

The man lauded as best ever to hold the office, and Fed Chairman during four presidencies (Ronald Reagan, George H. W. Bush, Bill Clinton, and George W. Bush) elegantly guided the United States through the Enron collapse, the dotcom bubble and the housing bubble, which caused the greatest depression since 1929.

And not a one of them did he see coming, which is his job. That’s an unprecedented run of failure compared with the office of any prior Fed Chairman.

One need no more evidence of his dimwittedness then that 2005 comment, that “These improvements have led to rapid growth in subprime mortgage lending; indeed, today subprime mortgages account for roughly 10 percent of the number of all mortgages outstanding, up from just 1 or 2 percent in the early 1990s.”

Well done, Alan. You pulled a cut-and-run by retiring just in time to dump all the rotten apples into Ben Bernanke’s lap.

Living to 100 was your penance…